[ad_1]

Second quarter earnings season is well under way, and its forming a positive counterpoint to a series of gloomy data releases expected this week. So far, some 100 or more of the S&P-listed firms have reported, and approximately 72% have been surprising to the upside. This runs counter to forecasts for later in this week – market watchers are expecting the Federal Reserve to bump up interest rates by another 0.75% on Wednesday, and are expecting Thursday’s Bureau of Economic Analysis release to show a contraction for Q2, which would put the US into a recession.

So which is it? Are we looking at earnings on the upside, or are we standing at the start of a recession? That may depend on the Federal Reserve; as the central bank pushes rates up to fight inflation, the higher cost of money of will put pressure on the economy, squeezing both jobs and GDP growth.

In a recent note to clients, Oppenheimer’s Chief Investment Strategist John Stoltzfus addresses these concerns. He writes, “Our view remains positive on the actions taken so far by the Federal Reserve since it pivoted in the fourth quarter of last year. We believe actions by the Fed leading to what we call ‘the end of free money’ to be a good thing for investors and the US economy. Too much liquidity in the system feeds speculation, overinvestment and distortion of valuations and expectations.”

“In our view, the Fed so far is doing the job that needs to be done while showing sensitivity to the near-term effects to the economy of its change in policy. Progress not perfection remains the order of the day in our view,” Stoltzfus added.

With Stoltzfus’ outlook in mind, we took a closer look at two stocks Oppenheimer is backing. The firm’s analysts see at least 60% upside potential in store for each. We used TipRanks platform to find out what the rest of the Street has to say.

Peloton Interactive (PTON)

The first Oppenheimer pick we’ll look at is Peloton, the interactive home workout company that reimagined home exercising, combining the venerable stationary bike with social media and digital video connections. The result: the creation of an online connected community, a feature that permits customers to participate in group exercise classes from their own living rooms or basements. This connectivity, which greatly benefited Peloton during the pandemic crisis, remains a major selling point for the company.

At the same time, the economic reopening of the past year has itself put pressure on Peloton. As customers got out more, there was less need for at-home exercise options, and Peloton’s financial results, which showed gains through the first three quarters of fiscal year 2021, have stuttered. Revenues fell back from 3Q21’s high point of $1.26 billion, and earnings have turned deeply negative.

In the most recent quarter, Q3 of fiscal year 2022, the company showed $964.3 million at the top line, down 23% year-over-year. Earnings, which registered a 3-cent per share loss in the year ago quarter, declined into a much deeper EPS loss of $2.27 – and even worse, coming in below the $83-cent forecast. Keeping this in the background, PTON’s share decline – some 73% year-to-date – makes better sense.

On a positive note, the company has seen its total members number rise steadily in recent quarters, from 5.4 million in fiscal 3Q21 to 7 million in fiscal 3Q22.

Oppenheimer’s 5-star analyst Brian Nagel, who holds the #34 spot in the TipRanks database, describes Peloton as ‘down but not out.’

Laying out this case, Nagel writes: “The past several quarters have proven tumultuous for Peloton, and its shares, as the story has morphed rapidly from promising tech unicorn, to COVID-19 winner, to post-pandemic victim. Through the lens of analysts with long-standing backgrounds in consumer and fitness, we re-studied carefully PTON and the company’s unique business model. Significant challenges for Peloton remain. That said, we believe that within the dynamic and fragmented health and wellness segment, there exists opportunity for a better-managed and more-disciplined PTON. Our positive call on PTON is longer term and highly speculative in nature.”

Fitting for his optimism, Nagel rates PTON shares as Outperform (i.e. Buy), with a $20 price tag that implies a strong upside of 109% for the year ahead. (To watch Nagel’s track record, click here)

The ‘longer term and high speculative’ nature of the Peloton as an investment, as well as its underlying strength, is clear from the Wall Street consensus. The stock has picked up 27 analyst reviews in recent weeks and months, and these include 14 Buys, 11 Holds, and 2 Sells, for a Moderate Buy consensus rating. Shares are trading for $9.55 and their average target of $21.04 suggests a one-year upside potential of 120%. (See Peloton stock forecast on TipRanks)

XPO Logistics (XPO)

The second stock on Oppenheimer’s radar is a trucking and transport company, XPO Logistics. This firm, based in Connecticut, is a major operator in the freight haulage business, and also acts as a transport broker. The core of the company’s business is its less-than-truckload freight segment, which operates globally – and in North America can reach into 99% of all US postal zip codes as well as significant areas of both Canada and Mexico.

XPO’s transport brokerage business is at the center of the company’s plans for streamlining; XPO will be spinning this segment off as a separate public entity this year. The new transport broker company, which will do business in a tech-enabled model, will be called RXO, while XPO will remain the moniker of the LTL and haulage segment, as a pure-play trucker. The spin-off is expected to be completed during the fourth quarter.

In the meantime, XPO is facing multiple headwinds that have put downward pressure on the shares. The cost of diesel fuel is up by a whopping 76% in the past year, and that has investors worried. The stock is down this by 30%.

At the same time, XPO’s financial results have been sound. The company will report Q2 results on August 4, but we can look back at Q1 for a sense of where this logistics company stands.

It stands on solid ground. The Q1 top line hit a company record of $3.47 billion, up nearly a half-billion, or 16%, from the year-ago quarter. Diluted EPS also rose year-over-year, posting a gain of 56 cents per share to reach $4.23.

For Oppenheimer’s Scott Schneeberger, another of the firm’s 5-star analysts, this all adds up to a stock that investors need to watch.

“We view XPO and its entry point attractive ahead of its 8/4/22 2Q22 earnings release, the possible sale/listing of its European Transportation business, and its pending 4Q22 spin-off of RXO. We’re comfortably maintaining our 2Q22E adjusted EBITDA of $365M (+10% y/y; $360-370M guidance; $364M consensus) following industry checks,” Schneeberger opined.

“We believe XPO’s North American LTL profitability initiatives are on-track, while its North American Truck Brokerage business, the cornerstone component of the pending RXO spin-off, has historically outperformed industry trends. We view the prevailing level of economic uncertainty as more than fully baked-into XPO’s current valuation vs. meaningful upside potential upon execution of its strategic objectives,” the analyst continued.

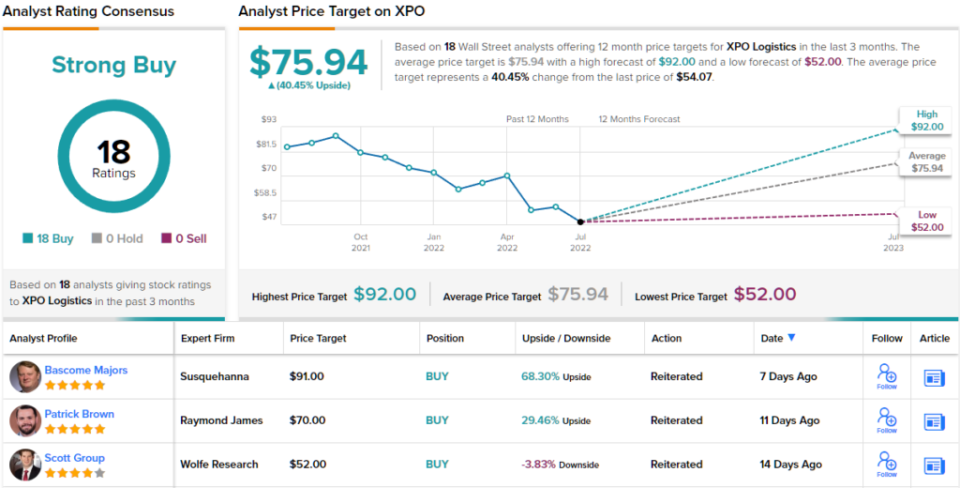

To this end, Schneeberger rates XPO shares an Outperform (i.e. Buy), unsurprisingly in light of his comments, and sets an $87 price target that suggests a robust 61% one-year upside for the stock. (To watch Schneeberger’s track record, click here)

It’s not often that the analysts all agree on a stock, so when it does happen, take note. XPO’s Strong Buy consensus rating is based on a unanimous 18 Buys. The stock’s $75.94 average price target suggests ~40% from the current share price of $54.07. (See XPO stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Source link