From Struggling to Recovering: The stats that specify why the UK music business is ready for a dramatic post-lockdown comeback.

[ad_1]

The next MBW evaluation comes from Will Web page, the writer of Tarzan Economics: Eight Ideas of Pivoting By means of Disruption. Web page (pictured) was beforehand the Chief Economist of Spotify and PRS for Music.

‘Ships passing one another within the evening’ is how I described Britain’s reside and recorded music industries in a Billboard article through the darkish days of lockdown, June 2020.

Streaming had turn into a ‘keep at house inventory’, entrance loading progress in subscribers and streaming volumes. In contrast, reside music had been all however silenced by the restrictions placed on our freedoms to curtail the pandemic.

That article supplied the proof base to assist policymakers, and contributed to the UK Authorities announcing a GBP £1.6 billion funding package for the humanities the next month, after which the UK Authorities launching a £750 million insurance scheme for reside occasions the next yr.

What issues, as one Scottish Chancellor consistently instructed me, is ‘evidence-based coverage making, not policy-based proof making’.

I used to be indebted to the UK’s PRS for Music, which licences reside occasions in order that its songwriter members can accumulate efficiency royalties when their songs are performed at live shows.

Its information on the British market, mixed with information on recorded-music spending by the Entertainment Retailers’ Association, allowed me to mannequin shopper spend throughout a time of disaster.

Now, they’ve let me replace the evaluation.

The unique insights garnered from this work are jaw-dropping. Buckle up.

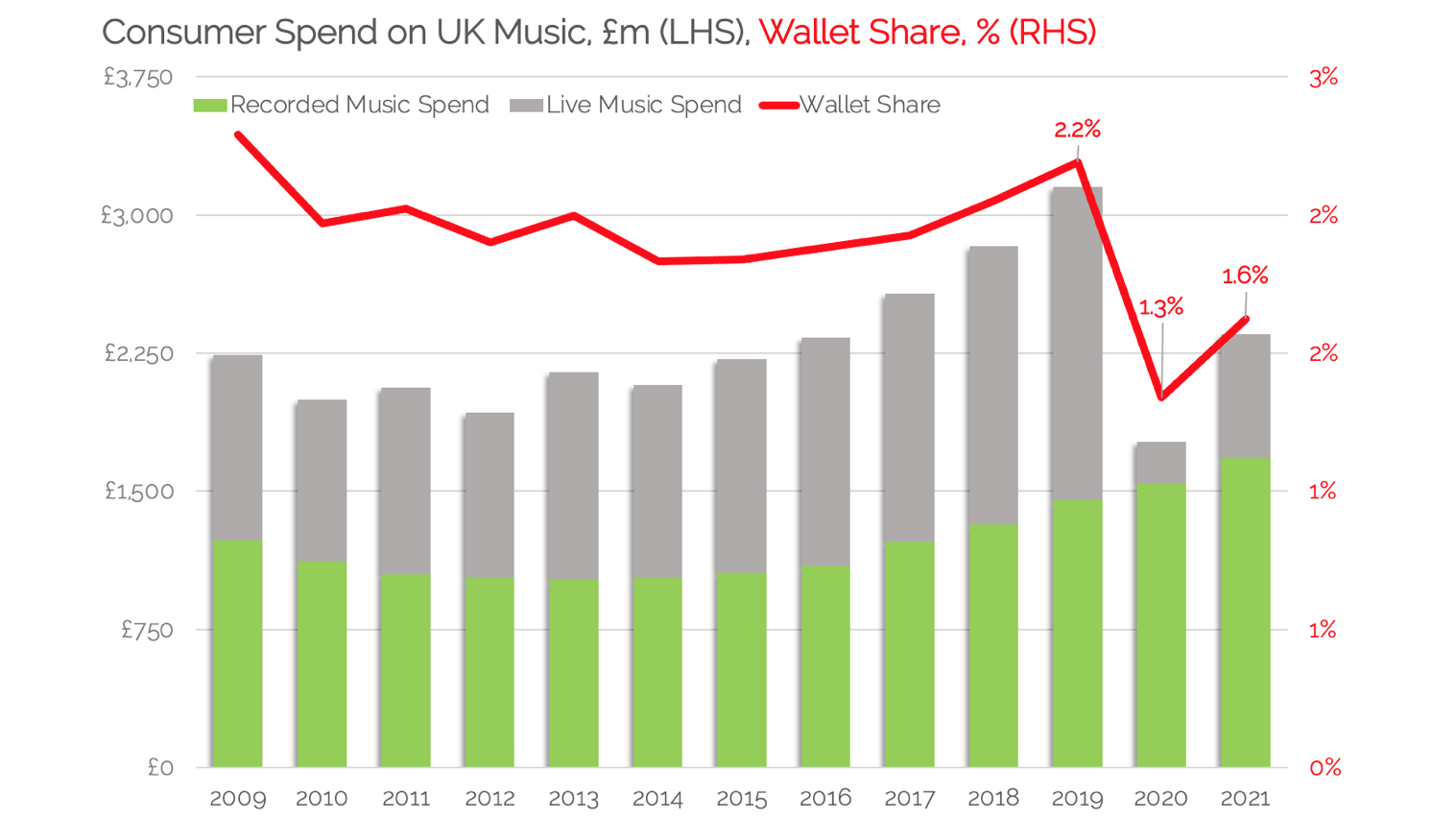

Stay vs recorded music spend. (Anybody bear in mind 2019?)

Let’s return to when the world was regular.

In 2019, British gig-goers spent GBP £1.7 billion on live performance tickets (or ‘field workplace’), a fifth greater than the £1.4 billion that customers spent on recorded music in the identical 12 months.

Mixed, British music followers spent a complete of £3.1 billion on music in 2019.

(Additionally: this live performance spend captures solely the first ticketing market — what’s generally often called the ‘face worth’ – and ignores secondary markets and ancillary spend.)

Then, music was silenced from our stage, however surged on our telephones.

Within the surreal yr of 2020, ‘field workplace’ collapsed 90% within the UK to only £200 million – whereas spending on recorded music accelerated by 6% to breach the £1.5 billion watermark.

As lockdown eased in 2021, streaming’s success continued, pushing UK recorded music spend nearer to £1.7 billion (paradoxically, the identical worth of the UK field workplace earlier than the pandemic), whereas reside spend recovered a few of its losses capturing £700 million in field workplace (nonetheless lower than half what it as soon as was).

The significance of ‘pockets share’ – and the way UK customers spend simply 0.2% of their cash on music

We will stack each parts of the British music business on prime of each other and add a last piece of the puzzle: pockets share.

The group on the Workplace of Nationwide Statistics who studied Covid’s impact on UK consumer spend kindly supplied me with information on recreation and tradition spend. This enabled me to measure whole UK spend on music as a share of what’s usually termed ‘the leisure greenback’.

Take into consideration this for a wee minute: one pound in each ten spent as we speak in Britain is on recreation and leisure – but solely two % of that leisure spend (which pans out as simply 0.2% of the grand whole) is spent on reside and recorded music.

Deflating, huh?

Now, let’s get to our chart.

On the left, spend on recorded music in inexperienced, stacked with field workplace spend in gray. On the best, the crimson line represents the share of leisure spend.

The gin-and-tonic relationship of accelerating subscriptions driving rising gig-going elevated pockets share from 2% in 2015 to 2.2% in 2019 – an even bigger share of an even bigger pockets.

As lockdown hit in 2020, wallets contracted and pockets share sank to 1.3% (much less share of much less cash), recovering to 1.6% final yr.

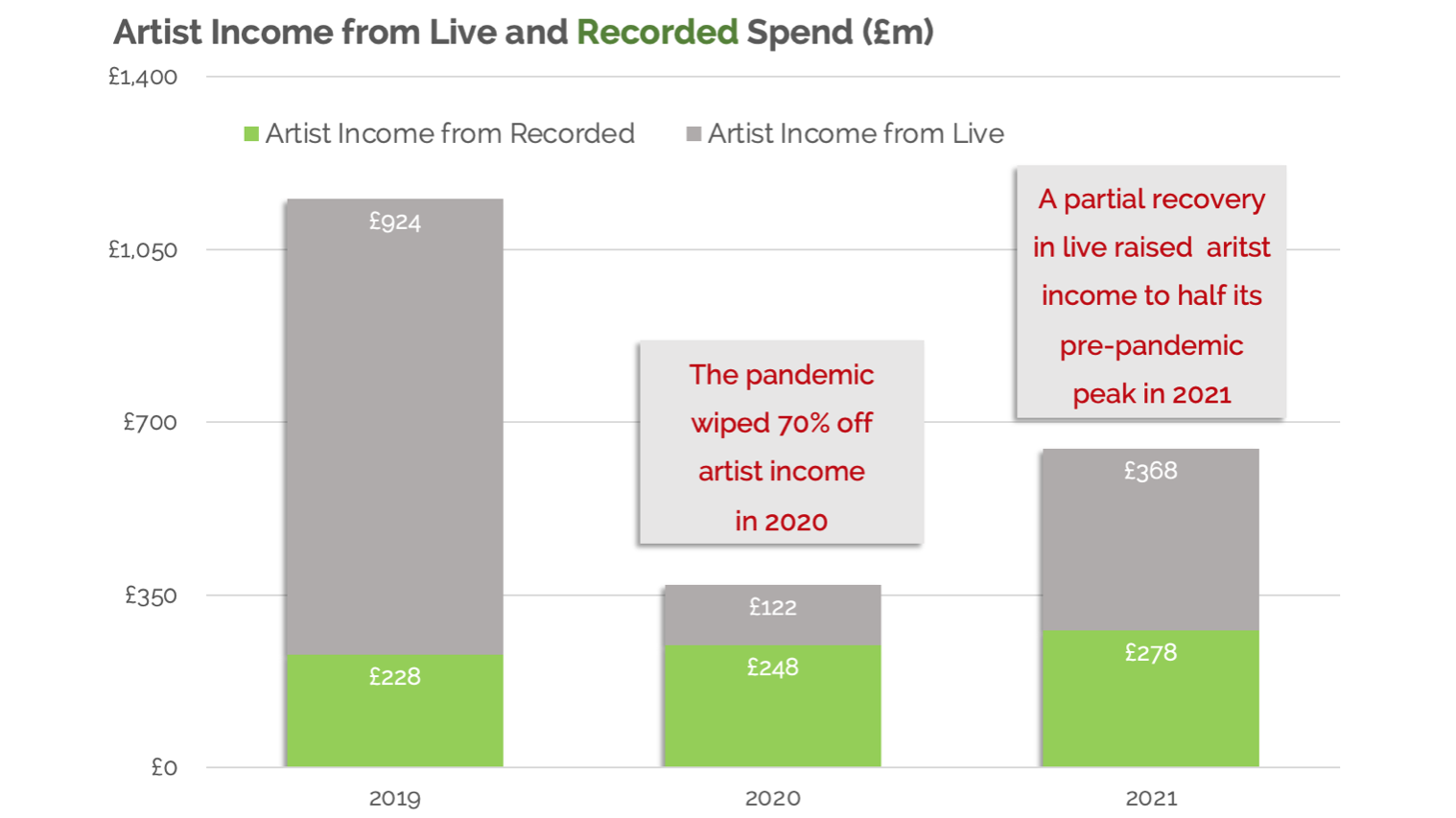

Now let’s determine what these lofty figures imply for artists.

For reside music, we strip out charges and taxes from the face worth of the ticket and provides the artist 75% of what’s remaining.

For recorded music we take the label’s personal wholesale worth of music and provides the artist 25%.

Bizarrely, these assumptions throw up an 80/20 rule for 2019: 80% of artist earnings got here from gigs, and 20% from recordings.

As reside music is the principle breadwinner for many artists, its silencing in 2020 overshadowed streaming progress, wiping 70% off their earnings.

If artists have been struggling to make a dwelling earlier than we locked down the UK financial system, then they’d 70% much less to make a dwelling after.

And in 2021, the partial restoration in reside and continued progress in streaming bought artist earnings to solely half what it as soon as was. For particular person artists, (much less so for corporations), that’s actually robust.

Whereas there’s no such factor as an ‘common artist’, a median pay lower of 70% raises questions of survival.

In 2019, reside music earnings was greater (and distributed among the many few) whereas recorded music earnings was smaller (and distributed amongst the numerous).

The pandemic immediately modified that blend.

As streaming has many more mouths to feed – and there’s nothing else to feed them with – it’s little shock that the UK business dragged itself by means of an arduous Parliamentary Inquiry through the lockdown years.

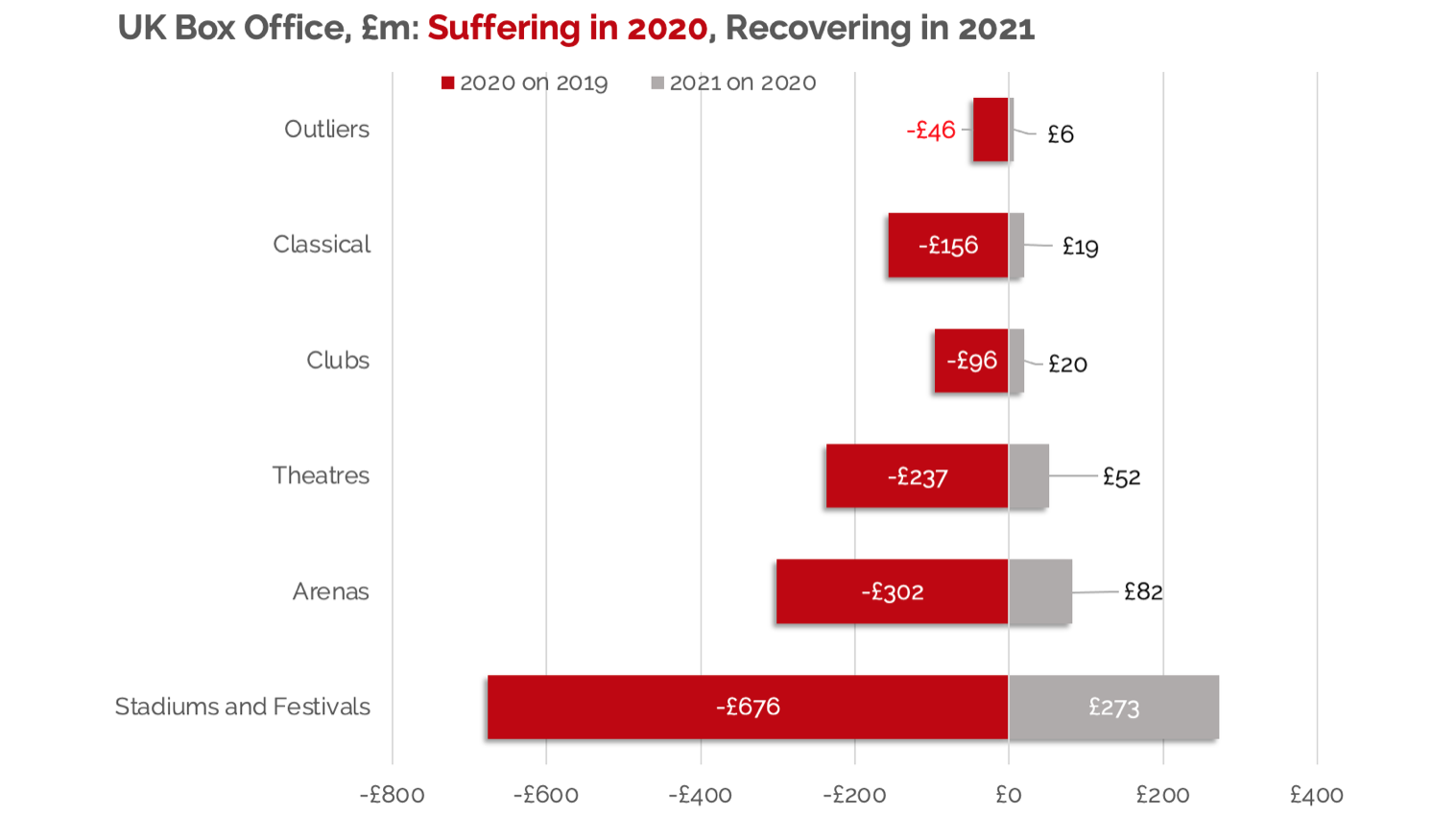

Now let’s concentrate on the ‘struggling and restoration’ in reside music.

In a New Year essay I confirmed that, for the reason that London Olympics, all the expansion in UK reside music was contained inside stadiums and festivals – rising their share from 23% in 2012 to 40% in 2019.

That’s on the expense of theatres, golf equipment and grassroots venues which have felt squeezed out of the British market, in absolute and relative phrases.

The chart under neatly illustrates that the more durable they arrive, the more durable they fall: Stadiums and festivals misplaced extra field workplace spend than arenas, theatres and golf equipment mixed in 2020, decreasing their share of UK field workplace all the way down to a measly 10 %.

From growth to bust to growth once more, 2021 noticed these out of doors occasions develop field workplace by over quarter of a billion, elevating their share of field workplace to a record-breaking 45%.

To make use of ‘lengthy tail’ language, the UK reside business has by no means been so ‘hit heavy’ – the place the spoils go to so few occasions.

The place we go now

These insights, unique to Music Business Worldwide, throw up questions {that a} world business can be taught from.

- First, how much does scale matter within the restoration? Bigger occasions owned by bigger corporations could have been higher capable of adjust to the shifting goal of presidency laws.

- Second, did journey restrictions give UK artists a leg-up within the UK pageant rankings and in that case, will it final?

- Third, we’ve had two years of keep at house ‘sofa-inertia’ (that’s Netflix and Pringles to you and me) so what’s going to it take for behaviours to alter and get us off our sofas and again into music venues?

Certain, we’re nonetheless a great distance off our pre-pandemic peak of £3.2bn shopper spend and a pair of.2% share of pockets.

However again to Gordon Brown’s level about evidence-based coverage making (and never policy-based proof making), this work offers policymakers and business professionals the mandatory basis to determine what help and actions are required to get us again to the place we as soon as belonged.

This isn’t going to be simple.

Wallets are set to be squeezed additional this yr and subsequent. That mentioned, with the internecine nature of the Parliamentary Inquiry behind us, the crucial is for all of us – policymakers, professionals and performers – to return collectively to unlock the ‘coiled spring’ demand for music on British levels up and down the nation.

James Taylor [not that one!] heads up music for Wembley Stadium. He sees this coiled spring(ing) into motion: this summer season, a record-breaking 16 live shows are happening on the well-known stadium with a staggering 1.3 million tickets bought; that’s the population of Edinburgh and Glasgow, mixed!

Now the mud has settled, let’s remind ourselves that music is the alchemy within the room that brings us collectively. And with the pandemic lastly behind us, these rooms will certainly be packed to capability.

If the collective ‘we’ get this proper, it’ll be extra like a slingshot than a rebound.

The writer want to thank: John Mottram and Frances Hodgson (PRSforMusic); Katherine Kent and Luke Croydon (Workplace of Nationwide Statistics), Liz Martins (HSBC Economics), Tim Chambers, Invoice Gorjance, Ralph Simon, Leisure Retailers Affiliation and the BPI.

He would additionally wish to share his due to DICE for his or her complete information on the UK reside occasions business.

Will Web page’s Tarzan Economics: Eight Principles of Pivoting Through Disruption (pictured inset) is out now through Simon & Schuster (UK) and Little, Brown and Firm (US).Music Enterprise Worldwide

Source link