[ad_1]

Is the bear market over? That is the query that everybody needs to know.

After a near-historic decline over the primary half of the 12 months, the inventory market has been on a roll over the previous month, with the S&P 500 rising practically 9%, whereas the Nasdaq is up 14%.

JPMorgan chief world markets strategist Marko Kolanovic has an upbeat message for these involved in regards to the sustainability of the rally.

“Threat markets are rallying regardless of some disappointing knowledge releases, indicating dangerous information was already anticipated/priced in… Though the exercise outlook stays difficult, we consider that the risk-reward for equities is trying extra engaging as we transfer via 2H,” Kolanovic opined.

In opposition to this backdrop, the analysts on the banking large have pinpointed two names which they consider are able to surge forward – by the order of 40% or extra. In reality, the JPM consultants are usually not the one ones singing these shares’ praises. In accordance with the TipRanks platform – they’re rated as Robust Buys by the Avenue’s analysts. Let’s take a more in-depth look.

Olin (OLN)

We’ll start with Olin, an organization whose roots stretch again all the way in which to 1892 when it was a small provider of blasting powder. Since then, it has grown considerably to turn into a worldwide producer and distributor of chemical merchandise. In reality, it’s now the world’s greatest producer of chlorine and caustic soda and their derivatives, and with a ~6% market share, takes the number one spot within the world chlorine/caustic soda market.

Towards the top of final month, Olin launched its newest quarterly report – for 2Q22. Income elevated by 18% year-over-year to $2.62 billion, whereas the corporate delivered diluted EPS of $2.76, beating the Avenue’s name for $2.57. However past the headline numbers, of explicit curiosity to shareholders, is the corporate’s buyback exercise.

Having rehabilitated its steadiness sheet in 2021, the corporate is now utilizing its money movement for the benefit of its shareholders, and aggressively shrinking the share base. The corporate repurchased 7.4 million shares in Q2, allocating $426.5 million to the endeavor, and mixed with Q1’s purchases, spent $689.7 million on buybacks in the course of the 12 months’s first half.

With a brand new $2 billion share repurchase program simply introduced that enhances the $362.5 million left over from a previous program, these buys inform J.P. Morgan’s Jeffrey Zekauskas’ bullish take.

“We estimate that Olin will spend $1.4b this 12 months on share repurchases,” the analyst writes. “Olin is conducting its share repurchase effort with free money movement and isn’t using monetary leverage. We additionally see no purpose why this sample of repurchase won’t proceed on the identical price in 2023 or in future years, if Olin’s share worth doesn’t transfer meaningfully increased. That mentioned, we consider that Olin is comfy with repurchasing its shares no less than into the mid-$60s based mostly on its public feedback.”

To this finish, Zekauskas charges Olin shares an Chubby (i.e., Purchase), whereas his $85 worth goal makes room for share appreciation of ~67%. (To observe Zekauskas’ monitor document, click here)

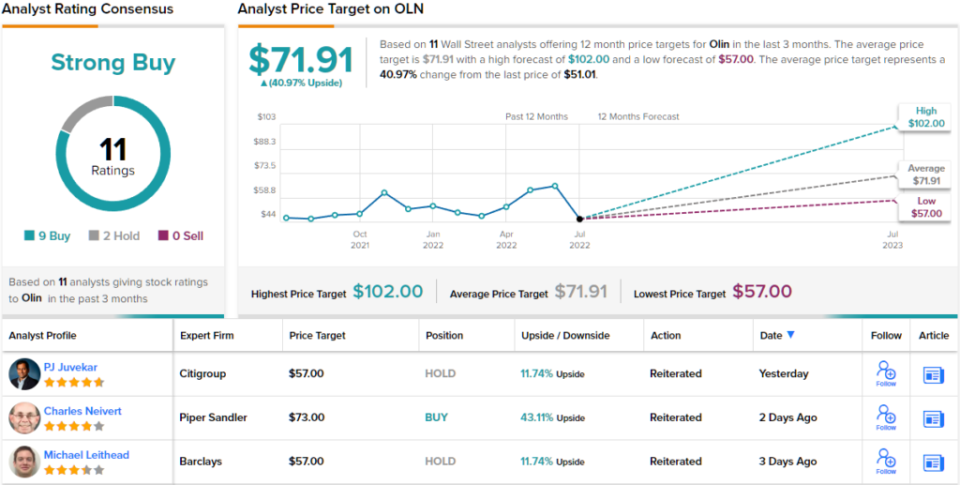

Total, Olin shares have a Robust Purchase ranking from the analyst consensus, displaying that Wall Avenue agrees with Zekauskas’ evaluation. The ranking is predicated on 9 Buys and a pair of Holds set previously 3 months. Shares are promoting for $51.01, and the typical worth goal, at $71.91, implies ~41% upside potential. (See Olin stock forecast on TipRanks)

GFL Environmental (GFL)

From chemical merchandise it’s only a quick hop to waste administration providers. GFL – which stands for inexperienced for all times – offers waste options and soil remediation providers. The corporate caters to residential, municipal, industrial, industrial and institutional purchasers unfold throughout Canada and has clients in additional than half of the U.S. states. With over 19,000 workers, GFL is North America’s fourth greatest diversified environmental providers firm.

The corporate has been very busy on the acquisition entrance, making 28 tuck-in acquisitions for the reason that begin of the 12 months, not that it appears to have a big destructive impression on the bottom-line.

Within the current Q2 report, adj. EBITDA got here in at C$453 million, easing forward of the $C$427 million anticipated by Wall Avenue. The highest-line efficiency enhances the earnings profile; revenues had been C$1.708 billion, additionally coming in above the consensus estimate of C$1.559 billion.

Extra excellent news was provided with the outlook, as the corporate raised its 2022 income steerage by C$400 million on the midpoint whereas additionally growing its adjusted EBITDA forecast by $20 million on the mid-point.

Though J.P. Morgan’s Stephanie Yee notes the impression prices are having on margins, she sees sufficient different constructive to maintain the bull thesis intact.

“Administration continues to see alternatives for extra tuck-in offers to densify the corporate’s footprint,” Yee writes. “Whereas the associated fee headwinds have pushed out the corporate’s timeline in direction of acquiring increased margins, we nonetheless see the general enterprise rising double digits in 2022 and high-single-digits in 2023, producing extra {dollars} that may be put to work. We additionally see the inventory as attractively valued at present ranges.”

These feedback underpin Yee’s Chubby (i.e. Purchase) ranking and $42 worth goal. Ought to the determine be met, buyers will likely be sitting on returns of 47% a 12 months from now. (To observe Yee’s monitor document, click here)

And what about the remainder of the Avenue? Everyone seems to be on board. The inventory boasts a Robust Purchase consensus ranking, based mostly on a unanimous 8 Buys. The forecast requires 12-month positive aspects of 39%, contemplating the typical worth goal stands at $39.65. (See GFL stock forecast on TipRanks)

To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Best Stocks to Buy, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely necessary to do your personal evaluation earlier than making any funding.

Source link